5 Myths About Wealth The Middle Class Still Believes (And Pay For)

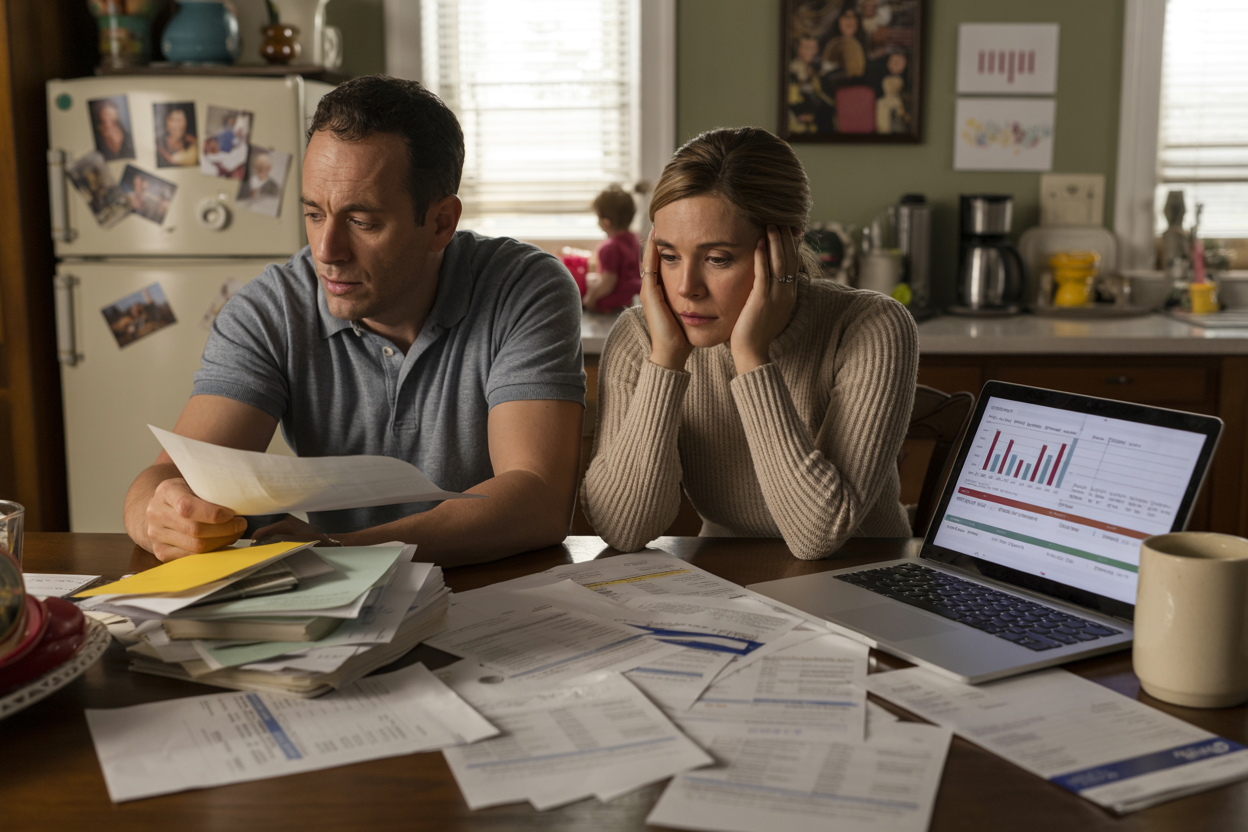

The middle class works hard, earns regularly and often feels like they are progressing financially. But the results tell a different story. Most households remain stuck in the same economic situation for decades, not because they lack effort, but because they follow culturally accepted myths that quietly drain wealth before it can accumulate.

These beliefs seem reasonable in the moment, but they create long-term damage that is difficult to reverse. Here are five myths about wealth that the middle class still believes and constantly pays for.

1. Higher income automatically makes you rich

Income creates the illusion of forward momentum. A raise feels like progress, a promotion feels like success, and a six-figure salary feels like you’ve arrived. But wealth is not built from what you earn. It’s built from what you keep, invest in, and let grow over time.

The problem is lifestyle inflation. Most people increase their spending in direct proportion to income growth, sometimes faster. The new car, bigger house, private school tuition and improved vacation time absorb the increase before it even hits a brokerage account. The result is higher income with no change in net worth. You run faster on the same treadmill.

High earners often remain financially fragile because their high lifestyles result in high fixed costs. When revenue stops or slows, the structure quickly collapses. The truly wealthy understand that income is a tool, not a goal. They convert income into assets that produce additional income. It’s the difference between simply making money and creating wealth.

2. My home is my greatest asset

The family home occupies a central place in the financial identity of the middle classes. This looks like an asset because the value shows up on net worth statements and the equity increases over time. But this framework ignores the real impact of the house on your cash flow and opportunity cost.

A primary residence is above all a shelter. This does not produce income. It consumes him. Property taxes, insurance, maintenance, utilities and mortgage interest create a constant cash outflow. Equity is illiquid, meaning it cannot be invested in productive investments without selling or borrowing. Meanwhile, capital tied up in home equity sits unused when it could have accumulated in the market.

The rich treat real estate differently. They buy income-generating real estate or keep their primary residence modest relative to their wealth so that capital can work elsewhere. Mistaking your home for an investment often means you’ve tied up your biggest equity in an asset that doesn’t earn you anything. It’s not about creating wealth. This is expensive storage.

3. Debt is OK as long as I can afford the payment

This is perhaps the costliest myth on the list. Focusing on monthly payments rather than total cost allows lenders to extend loans over longer terms, hide interest in the fine print, and sell you more than you can actually afford. The payment seems manageable, so the decision seems rational.

But interest is a slow leak that drains wealth over time. A $30,000 car financed at 7% over six years costs almost $35,000 after interest. This extra $5,000 could have been invested and capitalized. Consumer debt doesn’t just cost you the interest you pay. This costs you the returns you didn’t earn because that capital was allocated to servicing debt rather than growing assets.

The payment-first mentality also creates vulnerability. When cash flow tightens, these “manageable” payments become anchors. The rich either avoid consumer debt altogether or use it strategically and temporarily. They understand that every dollar spent on interest is a dollar that cannot benefit them. The middle class, on the other hand, finances a lifestyle and considers it normal.

4. I will invest more later when I earn more

This myth seems logical. It is responsible to wait until your income is higher before investing a lot of money. The problem is that time, not income, is the dominant variable in composition. Delaying investment is much more expensive than investing smaller amounts earlier.

Consider two investors. One starts investing $300 per month at age 25. Another waits until age 35, then invests $600 per month. Assuming an 8% annual return, the first investor ends up with much more in retirement despite having less total capital. The decade of capitalization of the first captured investor cannot be recovered by doubling contributions later. Time is an advantage that you cannot buy back.

The “later” mentality also ignores behavioral reality. When income increases, so do expenses. The surplus you expected never materializes as lifestyle adjusts upwards. Waiting to invest often means never investing at scale. The rich start early with what they have, even if it’s small. They understand that getting into the habit and capturing time is more valuable than waiting for perfect conditions that rarely arrive.

5. Looking rich means I’m doing well financially

Status spending is a wealth trap disguised as success. The luxury car in the driveway, the designer wardrobe, the exclusive zip code: all of these signal prosperity. But signaling prosperity and building prosperity are often opposing activities. One consumes capital, the other aggravates it.

Many high-income earners remain financially fragile because their ostentatious lifestyle eats up every dollar of excess income. They are housing rich and cash poor, or car rich and wallet poor. The appearance of wealth replaces real wealth, and the gap between the image and the balance sheet widens over time. When income slows or stops, the illusion quickly collapses because it has no basis.

The truly wealthy often deliberately live below their means. They drive older cars, avoid conspicuous consumption and invest the difference. They understand that every dollar spent on image is a dollar that cannot work for them. The middle class often does the opposite: spending to succeed in their projects while discreetly falling behind. Status is expensive, and the cost is financial independence.

Conclusion

The middle class does not fail because of a lack of discipline or effort. This approach fails because it follows culturally accepted financial narratives that seem reasonable but lead to poor long-term outcomes. These myths are everywhere: in social expectations, media messages, and casual financial advice. They are normalized, which makes them invisible.

Wealth is built by rejecting these myths early and consistently. This means prioritizing net worth over income, treating your home as a sanctuary rather than an investment, avoiding consumer debt altogether, investing immediately regardless of income level, and refusing to finance status. The gap between the middle class and the rich is not related to income. It’s a behavior. And behavior is a choice.

Berita Terkini

Berita Terbaru

Daftar Terbaru

News

Berita Terbaru

Flash News

RuangJP

Pemilu

Berita Terkini

Prediksi Bola

Technology

Otomotif

Berita Terbaru

Teknologi

Berita terkini

Berita Pemilu

Berita Teknologi

Hiburan

master Slote

Berita Terkini

Pendidikan

Resep

Jasa Backlink

Togel Deposit Pulsa

Daftar Judi Slot Online Terpercaya

Slot yang lagi gacor